The allure of remote institutional capital has transformed the retail trading space. Proprietary trading firms offer well-capitalized accounts to retail operators who can prove systematic execution consistency. Yet, despite advanced technical systems, over 90% of applicants fail evaluation phases within their first fourteen days. Strikingly, the vast majority of these accounts do not collapse due to deliberate, unhinged overtrading or chaotic margin allocation. Instead, they fall victim to an invisible algorithmic trap: the misunderstanding of daily drawdown calculations.

The Invisible Threat: Demystifying Prop Firm Risk Infrastructure

To survive in the modern capitalized evaluation environment, a professional operator must transcend basic chart reading and understand the programmatic risk parameters built into institutional risk engines. Prop firms do not evaluate accounts via human discretion; they run automated risk server loops that ping account parameters every few milliseconds. These algorithms track your balance and equity variations against rigorous mathematical thresholds designed to shield the firm’s pooled underlying liquidity from systemic market shocks.

The most devastating realization for retail traders is discovering that their account has been permanently deactivated for a daily drawdown breach during a session where every single closed trade resulted in a net financial profit. This paradox is not a software glitch—it is the direct outcome of how standard institutional metrics define daily boundaries. When your execution rules fail to account for floating valuation matrices, your portfolio is essentially exposed to unhedged termination traps.

The Two Mathematical Engines: Balance vs. Equity-Based Drawdown

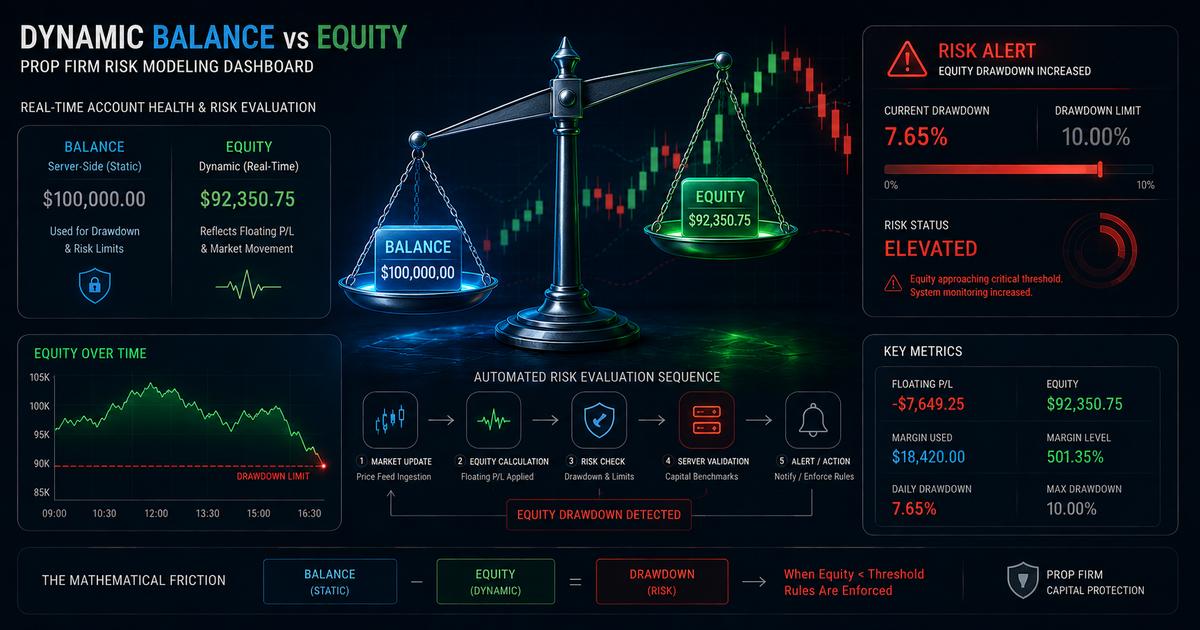

The architecture of daily risk parameters generally branches into two structural types. Understanding which configuration governs your evaluation account dictates how you must approach intra-session position tracking.

1. Balance-Based Daily Drawdown: This is the more forgiving infrastructure. The system logs your absolute cash balance at the exact moment of the daily server rollover clock (typically 00:00 CE(S)T or EST). If your starting balance is $100,000 with a 5% daily limit, your absolute maximum risk floor is locked at $95,000 until the next midnight reset. Floating profits that expand and collapse throughout the day do not alter this baseline, provided your equity never breaches that initial $95,000 floor.

2. Equity-Based Daily Drawdown: This is the highly sensitive mechanism utilized by industry giants like FundedNext and other modern evaluation platforms. The algorithm recalculates your daily threshold using whichever value is higher at the midnight reset: your closed balance or your floating equity. If you hold an open position running in massive profit as the clock strikes midnight, that peak floating equity is locked as your new daily high-water mark. The 5% allowed daily risk limit is then calculated downwards from that artificial peak, severely tightening your operational breathing room for the upcoming trading session.

The Mechanics of an Anatomy: How Good Traders Breach Rules Without Overtrading

Let us break down an empirical mathematical scenario to demonstrate how easily a conservative execution strategy can trigger an automated account termination sequence under an equity-based drawdown framework:

Imagine an optimized evaluation account with a starting balance of $100,000 and a strict maximum daily drawdown limit of 5% ($5,000). The trader executes a high-probability swing setup on GBPUSD ahead of a major macroeconomic release. The trade moves dramatically into profit, reaching a floating equity value of $106,000. The trader decides to hold the position overnight, expecting further continuation into the London open.

At 00:00 server time, the prop firm's risk engine captures the session snapshot. Because the equity ($106,000) is higher than the closed balance ($100,000), the system establishes $106,000 as the absolute baseline for the next twenty-four hours. Now, let us apply the 5% daily limit calculation:

Max Daily Loss Allowed: $106,000 × 0.05 = $5,300

Absolute Equity Breach Level: $106,000 - $5,300 = $100,700

The next morning, during the pre-market session, the GBPUSD position undergoes a completely normal 50% retracement of its previous impulse wave. The floating profit drops, causing the account's equity to fall from $106,000 down to $100,500. The trade is still technically in profit by $500 relative to the original entry point, and the trader's total balance remains pristine at $100,000.

However, because the current floating equity ($100,500) has dropped below the calculated daily boundary of $100,700, the prop firm's risk server registers an immediate rule violation. The trade is automatically liquidated, the account credentials are systematically revoked, and the evaluation fails. The trader is left bewildered—there was no overleveraging, no emotional revenge trading, and no violations of the ultimate trailing parameters. The account was destroyed entirely by a structural failure to track floating asset variances.

| Risk Variable | Balance-Based Model | Equity-Based Model |

|---|---|---|

| Calculation Baseline | Locked cash balance at 00:00 server time. | The higher value between balance or floating equity at 00:00 server time. |

| Impact of Floating Profits | Ignored by the daily tracking engine. | Locks in trailing peaks, raising your risk floor dynamically. |

| Overnight Holding Risk | Standard market gap and swap risk. | Extreme structural risk due to benchmark inflation. |

| Breach Triggers | Realized or floating losses breaching original baseline floor. | Any minor retracement of large open profits past midnight. |

Dynamic Exposure Control: Shielding Your Capital Against Server Rollovers

Mitigating this algorithmic trap requires transitioning from static position tracking to dynamic exposure mapping. The primary objective is to minimize the friction between your running positions and the midnight snapshot engine. If you find your current portfolio allocation struggling to recover from severe compounding mistakes under these stringent metrics, it is vital to review our master strategic framework on recovering from trading drawdowns to systematically realign your execution guidelines.

Professional capitalization operators employ two ironclad execution protocols to handle overnight market transitions:

- The Midnight Liquidation Rule: If you are executing setups under an equity-based prop firm framework, you must systematically flatten or aggressively scale out of floating positions at least fifteen minutes prior to the daily server reset. By converting floating profits into realized cash balances before midnight, you ensure your balance and equity remain uniform, preventing the calculation engine from creating an artificial trailing risk trap.

- Partial Trailing Stop Management: If a long-term position must be held over multiple sessions due to structural swing requirements, you must manually adjust your stop-loss order into locked profit. The protected stop value must be positioned at a level that guarantees even if the market triggers your stop during the next session, the resulting exit value stays safely above your daily breach floor.

Quantifying Asset Volatility via the Average True Range (ATR)

Another massive pitfall is treating different asset classes with identical leverage structures. Trading Gold (XAUUSD) or major currency pairs like GBPUSD requires drastically modified lot allocation models. Gold possesses an incredibly high-beta distribution profile, capable of multi-percentage intraday expansions that can wipe out an entire daily risk quota within a single 5-minute candle if your position sizing is unhedged. To understand how leverage can amplify these hazards into immediate margin liquidations, read our technical deep-dive explaining how leverage can become your trading enemy.

To mathematically combat asset volatility, you must track the 14-period Average True Range (ATR) on the Daily (D1) and Hourly (H1) timeframes. If Gold's current ATR is trading at historical highs, your position sizing must contract proportionally to ensure that a maximum adverse excursion across an average hourly range never exceeds 1.5% of your total account capitalization. This structural restriction ensures a protective buffer against unexpected daily rule triggers.

Eliminating Human Margin of Error via Systematic Calculators

Relying on mental calculations or manual approximations while trading volatile financial instruments under institutional observation is a recipe for catastrophic failure. The human brain is naturally poorly equipped to handle fractional compounding calculations under live market stress. Execution parameters must be verified via dedicated mathematical toolsets prior to executing any order.

Before risking your evaluation capital on a new position, you should feed your exact account parameters into our specialized Prop Firm Daily Drawdown Limit Calculator. This predictive component enables you to instantly parse your firm's specific balance or equity models, identify your exact risk floor for the current session, and derive the maximum lot allocation allowed for your protective stop-loss placement.

By taking a systematic approach, you bridge the gap between retail vulnerability and institutional execution discipline, ensuring your trading journey survives to harvest consistent long-term payouts.

Conclusion: Operational Checklist for Sustained Prop Account Capitalization

Conquering a proprietary firm evaluation phase has less to do with discoverable directional forecasting secrets and everything to do with flawless operational risk containment. To guarantee you never breach your daily drawdown allowances, commit this checklist to your daily routine: identify the firm's exact evaluation architecture, flatten or protect open positions prior to the midnight server rollover, size your trades dynamically based on real-time asset ATR metrics, and systematically run every setup through professional risk calculators. Treat risk as an exact science, and your equity curves will care for themselves.

Prop Firm Capital Preservation FAQ

What is the core difference between Balance-based and Equity-based daily drawdown?

Balance-based daily drawdown calculates your risk threshold using the fixed account balance at the start of the trading day (usually 00:00 CE(S)T). Equity-based drawdown updates dynamically based on your highest floating equity or balance at that specific moment. If you carry massive profitable floating positions past midnight, an equity-based system locks that peak value as the new benchmark, instantly tightening your risk profile for the next day.

Can a trader breach the daily drawdown rule without closing any losing trades?

Yes, absolutely. Under equity-based drawdown parameters, if your floating open positions experience a temporary retracement that exceeds the allowed daily percentage limit relative to your midnight equity baseline, the prop firm's automated risk server will instantly trigger a hard breach and liquidate the account, even if those positions ultimately revert to profit.

How does carrying open positions through the daily market close affect my drawdown limit?

Carrying open positions past the market reset time forces the risk engine to log your current floating valuation as the new baseline for the following day. If your floating equity is significantly higher than your balance, your daily maximum allowed loss for the next session is calculated from that inflated equity peak, exposing you to severe tracking risks if the market gaps or reverses.

Does the daily drawdown counter reset based on my local timezone or the prop firm server timezone?

The drawdown metric always resets precisely according to the proprietary trading firm's specific server clock, which is typically configured to Central European Time (CET/CEST) or Eastern Standard Time (EST) to match the New York/London market rollover periods. You must align your automated risk parameters with the server time rather than local execution metrics.

What is the safest way to mathematically ensure I never breach a daily loss limit?

The most effective method is utilizing automated execution scripts paired with a dynamic position sizing algorithm. By assessing the precise asset volatility (ATR) and entering calculations into a professional daily drawdown calculator, you can establish hard execution stop-losses that align with maximum daily capital risk thresholds, completely eliminating human operational errors.