Developing a robust algorithmic execution platform within MetaTrader 5 demands a fundamental transition from simplistic technical pattern recognition to rigorous, multi-variable quantitative engineering. While retail participants often construct single-timeframe Expert Advisors (EAs) that succumb to market noise, institutional algorithms look for macro alignment. This guide details the structural architecture required to engineer a production-ready, object-oriented MQL5 trend-following algorithm. By isolating directional market bias on the H1 timeframe using an Exponential Moving Average (EMA) filter and synchronizing execution entries via lower-timeframe M1 or M5 structures, we minimize false signals and mathematically optimize entry parameters.

The Structural Flaw in Single-Timeframe Automation

The fundamental failure vector for the majority of automated systems is localized market noise. In highly liquid, volatile arenas like the foreign exchange or spot commodity spaces, executing order entries based strictly on isolated lower-timeframe parameters introduces severe variance traps. A clean moving average crossover or momentum breakthrough on an M5 chart is often nothing more than a temporary liquidity sweep designed to fill larger institutional blocks resting on macro supply nodes.

To survive these anomalies, an automated system must feature a clear hierarchy of structural execution. The algorithm must restrict transaction permissions entirely unless lower-timeframe impulses are verified by higher-timeframe trends. If an algorithmic system operates without these parameters, its long-term equity profile is mathematical fuel for market makers. To see how unmitigated leverage models compound these execution errors under extreme market expansion, review our research on the mathematics of leverage collapse in retail trading portfolios.

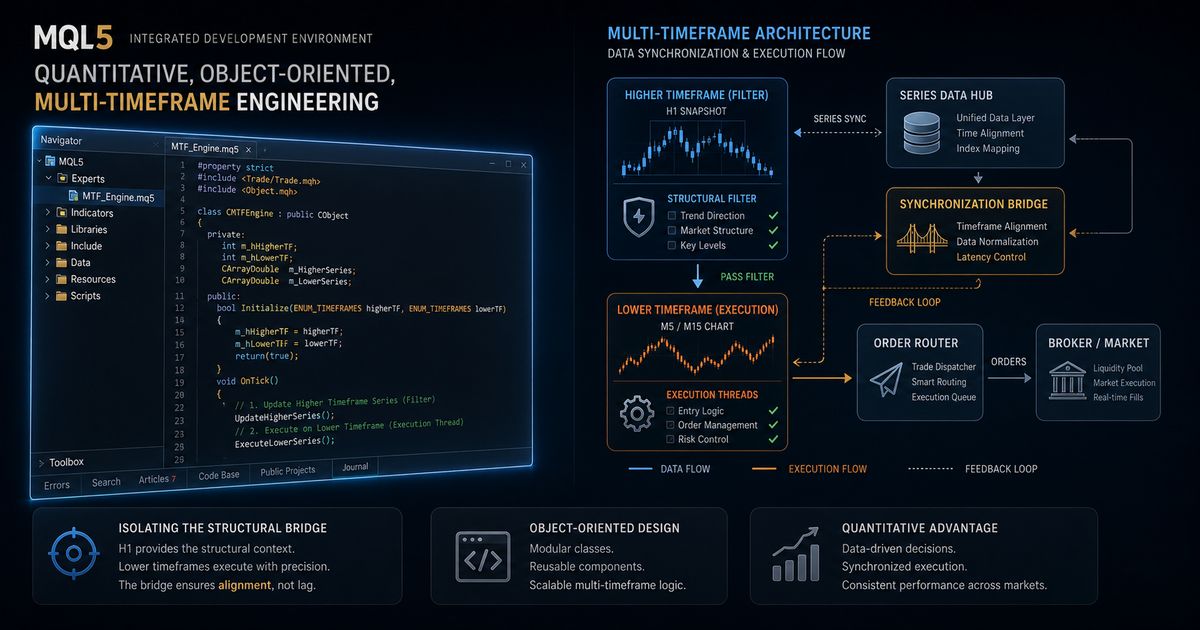

The Blueprint: H1 Bias Filtering + M1/M5 Execution Logic

Our systematic model divides the trading framework into two separate, asynchronous tasks:

- Macro Directional Filter (H1 Timeframe): The algorithm continuously tracks the 200-period Exponential Moving Average (EMA 200). If the closed price of the prior H1 bar rests completely above the EMA line, the core logic initializes a strict

BIAS_BUYstate. Conversely, if the price resides below, it enters aBIAS_SELLstate. - Micro Execution Engine (M1/M5 Timeframe): Once the global state variable is established, the low-timeframe engine scans for localized structural confirmations. It actively maps localized demand or supply zones, utilizing specific candle body and wick boundaries to trigger execution orders into the macro trend vector. For a complete programmatic deep-dive on locating these dynamic price structures, see our technical walkthrough on Mastering Structural Highs and Lows via iHighest and iLowest Functions in MQL5.

MQL5 Logic Structure: Multi-Timeframe Synchronization

Unlike legacy development environments, a modern production EA requires manual management of asynchronous data arrays, indicator handles, and structured buffer queries. The algorithmic framework must safely initialize distinct technical indicators during the setup block, handle live market data ticks, and copy array values dynamically using specialized memory arrays to avoid processing latency.

A professional-grade implementation enforces bar-boundary constraints, ensuring the execution engine checks parameters only upon the completed closure of a candlestick. This computational safeguard insulates the trading balance from real-time repainting issues, intra-bar whipsaws, and artificial execution triggers that degrade algorithmic performance during volatile trading sessions.

Furthermore, protective temporal constraints must be integrated to shield the trade routine from illiquid market shifts. To implement an optimized system lock that prevents entries during low-liquidity rollovers, check out our implementation code on Implementing MQL5 Algorithmic Time Filters to Avoid Friday Rollovers and Weekend Gaps.

The Asymmetric Core: Volatility Sizing Calibration

Writing optimized multi-timeframe filter parameters in MQL5 represents only half of the algorithmic survival matrix. An algorithm can feature a 70% precision win-rate, yet still experience devastating geometric decay if its trade-volume execution layer utilizes arbitrary or static lots. Because localized stop-loss sizes vary depending on low-timeframe wick configurations, lot sizes must scale dynamically.

To isolate account structures from sudden variance spikes—especially within aggressive commodity distributions like spot gold—automated platforms should verify variables using precision engines. Utilizing a dedicated Gold Position Size Calculator allows you to bridge structural stop boundaries with real-time balance calculations, preventing technical breaches before transmission.

For advanced developers managing accounts under rigorous prop firm evaluation criteria, calculating drawdown expansion is a fundamental requirement. If consecutive stop-outs occur within highly correlated market clusters, checking variables against a dynamic Prop Firm Drawdown Calculator protects your portfolio from hitting institutional liquidation thresholds.

Advanced Strategy: Multi-Series Synchronization Matrix

To visualize how structural bias thresholds interface across temporal windows, review our architectural liquidity delivery index:

| H1 Trend Filter Status | M1/M5 Local Structure | Execution Thread Action | Systemic Risk Rating |

|---|---|---|---|

| Price > EMA 200 (Bullish) | Demand Zone Validation / Candle High Breach | Execute BUY Order Thread | Low (High Probabilistic Synergy) |

| Price > EMA 200 (Bullish) | Supply Zone Invalidation Signal | ABORT / Restrict Sell Flags | Neutral (Noise Filtration Engaged) |

| Price < EMA 200 (Bearish) | Demand Zone Support Bounce | ABORT / Restrict Buy Flags | Moderate (Counter-Trend Whipsaw) |

| Price < EMA 200 (Bearish) | Supply Zone Validation / Candle Low Breach | Execute SELL Order Thread | Low (Trend Alignment Vector) |

Guarding the Execution: Spread and Slippage Mitigation

Even the most sophisticated multi-timeframe algorithm will fail if it is deployed without an explicit execution guard layer. During volatile market windows, such as the New York session roll-over, interbank liquidity pools temporarily evaporate. If your logic triggers an order during these windows, the trade engine will experience massive slippage.

To prevent this, you must integrate an analytical check prior to firing an order. If your account equity curves have sustained damage due to unmitigated execution fills within low-liquidity zones, reading our comprehensive recovery guide on recovering systematically from compounding drawdown phases is essential to restore your platform's mathematical edge.

Conclusion: The Imperative of Systematic Optimization

Transitioning to systematic MQL5 automation requires shifting your focus from chasing short-term market direction to protecting quantitative parameters. By binding entry layers to macro-aligned multi-timeframe filters, you insulate your capital from market noise and establish a repeatable framework for long-term survival in the algorithmic landscape.

Never allow structural strategies to run untested against low-fidelity datasets. To verify your multi-timeframe dependencies without modeling flaws, read our institutional blueprint on Achieving 99.9% Backtesting Accuracy via MT5 Real Ticks Environment to secure historical consistency before applying live capital allocations.

Quantitative MQL5 Development FAQ

How do you handle multi-timeframe indicator data asynchronously in MQL5 without freezing the execution thread?

In MQL5, asynchronous data pooling is handled correctly by initializing distinct indicator handles using iEMA or iCustom during OnInit(). Within the OnTick() loop, developers must employ CopyBuffer() to selectively retrieve only the historical arrays required, wrapped in validation blocks to ensure the target timeframe series has completely synchronized with the MetaTrader server.

Why is structural bar-boundary execution preferred over tick-by-tick evaluation for MTF algorithms?

Evaluating high-timeframe parameters (like H1 EMA bias) on every incoming tick is computationally inefficient and introduces market noise latency. Executing trade logic on the close of the bar ensures structural boundaries are mathematically locked, eliminating real-time repainting issues and stabilizing backtesting accuracy.

What is the optimal method to calculate dynamic stop losses based on technical structures in MQL5?

The optimal method is utilizing specialized candle boundary logic. For a buy order, the algorithm scans a predefined historical array loop to identify the lowest wick price of a candle pair or demand zone, subsequently setting the hard Stop Loss at that precise level while cross-referencing position risk via quantitative models.

How do you prevent trade placement when historical spread deltas expand?

By querying SymbolInfoInteger(_Symbol, SYMBOL_SPREAD) before sending an OrderSend() request. If the live spread exceeds your predefined threshold or statistical average, the execution block is aborted, insulating your capital from toxic slippage during high-volatility roll-overs.

Why do many trend-following algorithms suffer from catastrophic geometric degradation?

Geometric degradation is typically not a flaw of the signal generation itself, but a byproduct of faulty position sizing models. Running static lot setups across varied volatility expansions causes asymmetrical capital loss during inevitable consecutive losing streaks.