The most hazardous stage of algorithmic development isn't debugging syntax errors—it is surviving backtesting delusions. Many developers build robust, multi-timeframe Expert Advisors only to be blinded by spectacular backtesting curves that immediately degrade when deployed onto live capital infrastructure. This systemic variance is usually not caused by faulty trade logic, but by poor modeling quality settings. While legacy platforms forced developers to rely on complex third-party scripts to achieve high fidelity, MetaTrader 5 introduces native access to institutional-grade optimization via its "Every tick based on real ticks" engine.

The Backtesting Illusion: Generated Ticks vs. Real Ticks

To optimize processing overhead, standard retail backtesting models utilize mathematical shortcuts. In the default Every Tick environment, the Strategy Tester doesn't parse actual transactional data. Instead, it references historical M1 OHLC bar boundaries and uses a fractal formula to generate artificial price points inside the candle.

While this method is sufficient for simple swing systems, it fails completely when evaluating advanced algorithms. Quantitative engines—especially those relying on multi-timeframe alignments or custom stop calculations—are highly sensitive to intra-candle price sequence variations. Simulated ticks obscure real-world execution factors like variable spread widening during data roll-overs, institutional liquidity sweeps, and sudden stop-out gaps.

The Multi-Timeframe Synchronization Vulnerability

As detailed in our structural benchmark article, Building a Trend-Following Algorithm: Multi-Timeframe EMA Filters in MQL5, a production EA continuously evaluates macro directional parameters (like the H1 EMA 200) alongside lower execution windows (M1/M5 charts).

If you test such an architecture without real tick synchronization, the Strategy Tester synchronizes historical bar open times perfectly on paper, but completely misses the actual sub-second order book updates. This data mismatch introduces artificial repainting anomalies—causing indicators to look ahead in time during backtesting. This generates unrealistic profit profiles that vanish entirely when running on live interbank feeds.

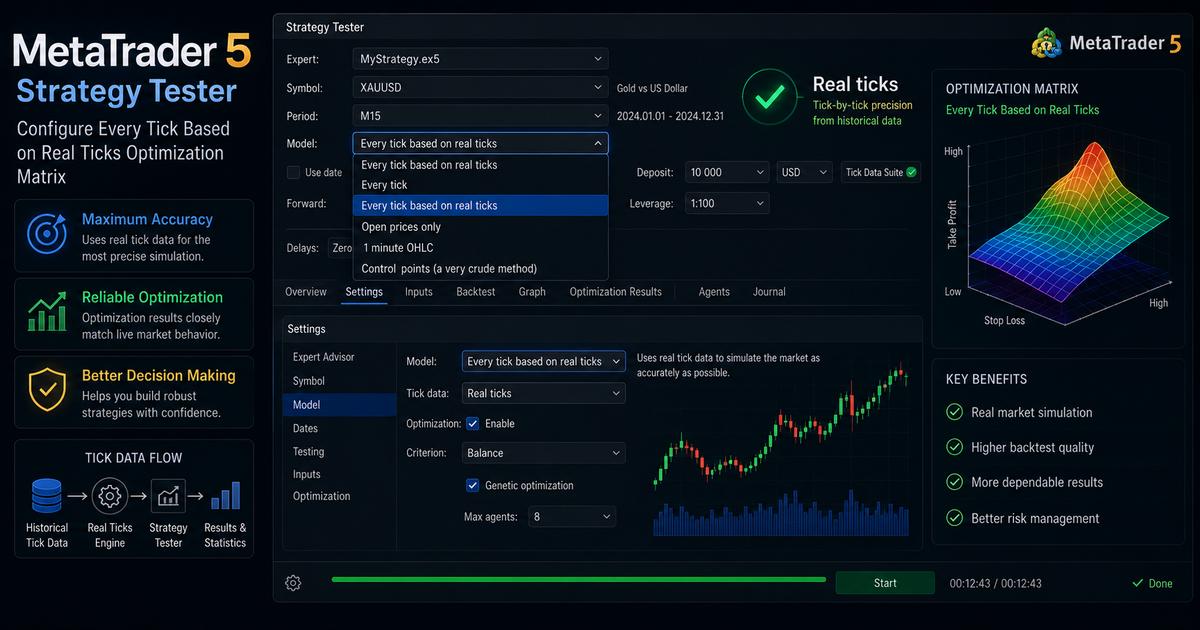

Step-by-Step Configuration for 99.9% Real Ticks Validation

To configure your MetaTrader 5 terminal for flawless data extraction, complete the following deployment steps:

- Acquire a Real-Tick Broker Data Feed: Ensure your underlying MT5 account is hosted by a prime brokerage that maintains deep historical tick databases on their infrastructure servers.

- Initialize the Strategy Tester Matrix: Press

Ctrl + Rto launch the diagnostic platform. Select your target compiled compiled.ex5Expert Advisor file. - Adjust Modeling Properties: Navigate to the Model configuration interface and select "Every tick based on real ticks".

- Enforce Variable Spread Realism: Set the spread tracking property to Variable. This forces the engine to replay the historical spread expansion records precisely as they occurred in live market sessions.

Programmatic Code Optimization for Historical Verification

To guarantee your MQL5 source code properly leverages high-fidelity data structures and handles real-world connectivity changes, add this programmatic synchronization check inside your core execution block:

//+------------------------------------------------------------------+

//| Verifies Data Buffer Synchronization Security Prior to Evaluation |

//+------------------------------------------------------------------+

bool IsHistoryBufferFullySynced(string assetSymbol, ENUM_TIMEFRAMES targetTimeframe)

{

// Query if the terminal has completely synchronized history caches with broker databases

if(!SeriesInfoInteger(assetSymbol, targetTimeframe, SERIES_SYNCHRONIZED))

{

Print("Database Latency Detected: Synchronizing historical series arrays for " + assetSymbol);

return false; // Interrupt execution loop to avoid processing uninitialized or faulty price frames

}

return true; // Historical validation completed successfully

}The Cost of Precision: Computational Realities

Transitioning to a 99.9% accuracy architecture involves a clear tradeoff: Execution Latency and Processing Overhead. Because the Strategy Tester must parse gigabytes of raw, sequence-accurate tick files instead of compressed M1 blocks, your optimization runs will take significantly longer.

To mitigate this processing bottleneck, developers should leverage MT5's multi-threaded testing capabilities, run local optimization passes using specialized OpenCL GPU pipelines, or distribute complex variable calculations across the decentralized MQL5 Cloud Network.

Data Modeling Quality Spectrum

Review the comparison matrix below to understand how varying modeling modes impact calculation accuracy and system performance:

| Modeling Selection Mode | Fidelity Index | Spread Simulation Profile | Recommended Use Case |

|---|---|---|---|

| Open Prices Only | Low (~25%) | Static / Fixed Matrix Only | Rapid rough-draft logic and syntax validation runs |

| Every Tick (Generated) | Moderate (~90%) | Static or Interpolated | Initial variable scanning and wide parameter filtering |

| Every Tick Based on Real Ticks | Maximum (99.9%) | Historical Variable Record | Final institutional validation before deploying live capital |

Conclusion: Protecting the Quantitative Edge

Algorithmic edge is rooted in mathematical consistency. If your optimization routines depend on simulated or artificial data, your system is built on a flawed foundation. By configuring your Strategy Tester to process actual historical broker transactions, you remove guesswork, unmask curve-fitting errors, and verify that your trend-following models possess a genuine statistical edge capable of enduring real-world live market conditions.

Quantitative Development FAQ

What distinguishes 'Every tick based on real ticks' from standard 'Every tick' modeling in MT5?

'Every tick' relies heavily on a mathematically generated fallback grid generated from historical M1 bars (fractal interpolation). Conversely, 'Every tick based on real ticks' downloads the actual historical transactional ticks recorded directly by the broker exchange, mapping exact historical spread fluctuations and floating slippage profiles perfectly.

Why do multi-timeframe algorithms fail when tested on lower modeling qualities?

Multi-timeframe algorithms require simultaneous synchronization across historical data buffers (e.g., matching M5 entries with H1 EMA trends). If standard M1 interpolation is used instead of real ticks, historical candle boundaries repaint inaccurately inside the Strategy Tester, generating artificial entry executions that are impossible to replicate in live market environments.