In the institutional landscape of professional asset allocation and modern proprietary trading evaluations, capital preservation is governed by rigid mathematical boundaries. While retail participants primarily focus on nominal win rates or localized technical setups, quantitative portfolio managers optimize for path dependency. The survival of a trading enterprise depends entirely on understanding how risk metrics are calculated by the clearing firm or funding institution. Misinterpreting the architectural difference between Relative Drawdown and Trailing Drawdown is one of the most common reasons quantitative strategies face sudden liquidation, even when operating with an historically positive mathematical expectancy.

The Anatomy of Capital Contraction Metrics

Drawdown, in its simplest mathematical formulation, defines the peak-to-trough decline of an account’s financial equity curve over a specific observation sequence. However, when transitioning into institutional frameworks or corporate evaluations, drawdown ceases to be a passive performance metric. Instead, it becomes an active execution barrier.

The risk profile of a portfolio is continuously assessed through real-time balance and equity streams. If a portfolio manager fails to program matching internal risk boundaries, localized volatility expansions can cause a terminal risk breach. This risk compounds rapidly when strategies run unmitigated leverage limits across high-beta assets. To avoid unexpected capital liquidation events, traders must carefully study how leverage can become your trading enemy when asset volatility spikes unexpectedly against your open exposures.

Deconstructing Relative Drawdown

Relative drawdown represents a dynamic percentage-based risk boundary calculated using either the initial starting balance or adjusted historical balance intervals. It is computed using the highest point the account balance has realized, scaling the absolute loss threshold relative to capital growth.

The core equation governing a standard relative valuation threshold can be modeled as follows:

Consider a portfolio with a starting balance of $100,000 and a strict 10% maximum relative drawdown constraint. The initial hard liquidation floor is established at exactly $90,000. If the portfolio generates realized gains, increasing the balance to $110,000, the relative drawdown floor scales proportionally upward, anchoring the new liquidation boundary at $99,000 ($110,000 minus 10%).

The critical operational parameter of relative drawdown is that it changes based on realized closed balances. If an open trade experiences intra-day variance but does not create a new permanent balance milestone, the baseline protection floor remains fixed at its last locked position.

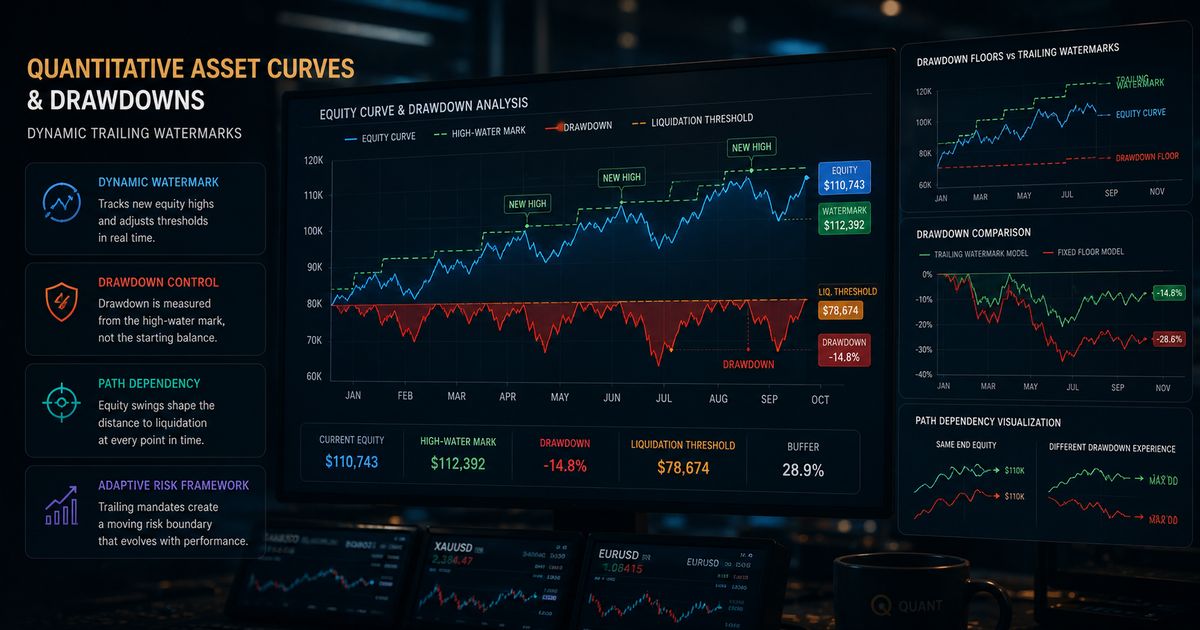

The Trailing Drawdown: The High-Water Mark Trap

The trailing drawdown model is an aggressive risk constraint favored by modern instant-funding institutions and futures prop firms. Unlike relative structures, a trailing drawdown does not wait for positions to close before adjusting its baseline. It recalculates the maximum allowed loss threshold dynamically in real-time, matching the peak high-water mark of your account's open floating equity.

This real-time adaptation introduces severe path dependency vulnerabilities. Let us analyze the operational mechanics across a live execution scenario:

- Initial Allocation State: A quantitative trader begins with a capital allocation of $100,000 with a 5% trailing drawdown limit. The hard liquidation threshold is initialized at $95,000.

- Open Profit Expansion: The trader executes a high-beta trade. The asset expands aggressively, pushing the account's open equity value to $106,000. Because the system tracks open equity peaks, the trailing threshold rises to $101,000 ($106,000 minus 5%).

- The Volatility Retracement: The position encounters an unexpected macroeconomic shift, and the open profit vanishes. The open equity pulls back from $106,000 to $101,500. Even though the realized account balance remains at its original $100,000 baseline, the active risk ceiling is locked at $101,000. The account is now less than $500 away from a terminal liquidation event.

Mathematical Modeling: The Probability of Systemic Ruin

To understand why trailing equity watermarks cause higher structural failure rates for retail practitioners, we can evaluate asset profiles through risk-of-ruin models. Because trailing parameters act as a one-way ratchet—moving upward with profit expansion but locking in place during drawdowns—they restrict the strategy's operational workspace.

The mathematical path to asset degradation increases significantly when an algorithmic system operates with wide stops and long holding horizons. If consecutive stop-outs occur within correlated asset clusters, the lack of buffer space leads directly to systemic termination. Portfolio operators can analyze these risk dynamics before launching models using our specialized Prop Firm Daily Drawdown Calculator. This tool maps variance structures to ensure your stop distances do not breach tracking rules during execution spikes.

When executing large order blocks on volatile assets, ensuring lot sizes are precisely calibrated is non-negotiable. If you deploy an automated model on gold without adjusting for contract variance, your floating high-water mark can rise and fall drastically within a single H1 bar. This movement can inadvertently ratchet up your trailing threshold and trigger a liquidation breach. To prevent this, integrate our specialized Gold Position Size Calculator to dynamically scale your risk parameters relative to your available drawdown balance.

"A trailing drawdown does not preserve capital for the trader; it converts unrealized upside volatility into realized structural risk."

Comparative Analysis Matrix: Evaluation Models

To help risk managers visualize these architectural variations across production accounts, we have structured an institutional comparative matrix:

| Risk Metric Variable | Relative Drawdown Model | Trailing Drawdown Model |

|---|---|---|

| Calculation Driver | Realized closed balances at session transitions. | Peak unrealized intra-trade equity values. |

| Threshold Movement | Adjusts exclusively upward when a new closed balance is locked. | Ratchets upward in real-time; never recalculates downward. |

| Impact of Open Profit | Neutral. Creates an extra protective cushion. | High Risk. Increases the hard liquidation floor. |

| Strategic Execution Fit | Swing strategies, longer-horizon trend execution. | High-frequency scalp execution, rapid target completions. |

Hedging the Architecture: Tactical Recovery Playbooks

Operating a systematic framework under trailing constraints requires adjusting your order management logic. Traditional buy-and-hold strategies or wide trailing stops are unviable because they naturally risk breathing room when profits retrace. Instead, quantitative developers must adjust their exit logic to prevent floating drawdowns from triggering liquidations.

If your portfolio has sustained structural damage due to unexpected trailing breaches, standard aggressive recovery models can accelerate account failure. Managing capital contraction requires a systematic approach. To restore your strategy's edge, consult our comprehensive guide on recovering systematically from compounding drawdown phases. This guide outlines how to realign position sizes during capital recovery periods.

Conclusion: Strategic Alignment for Long-Term Survival

Long-term trading success requires aligning your execution parameters with your account's strict structural constraints. If your trading platform is governed by relative metrics, you can utilize trend-following models with wider trailing targets. However, if you are bound by a real-time trailing equity high-water mark, you must adapt your execution logic. In this environment, you must implement tight partial take-profits and actively manage stops to protect your capital from sudden market reversals and avoid liquidation breaches.

Quantitative Drawdown Architecture FAQ

What is the primary operational difference between a static relative drawdown and an equity trailing drawdown?

Static relative drawdown calculates the threshold strictly from the initial deposit or a fixed balance point baseline. Conversely, an equity trailing drawdown recalculates the maximum permissible loss limit dynamically in real-time, matching the peak high-water mark of the account's open or closed equity and capturing floating profits as structural variance.

How does an open floating profit affect a trailing drawdown structure during high-volatility sessions?

Under an equity trailing drawdown model, if a position floats into a large profit but is not closed, the maximum liquidation threshold trails upward to lock behind that temporary peak. If the market aggressively reverses, the trader's effective risk parameter contracts dramatically, causing a breach even if the nominal absolute account balance remains positive.

Can a trader experience a liquidation breach under trailing constraints while having zero closed losing trades?

Yes. If an open trade prints a major upward variance peak and subsequently retraces past the trailing distance constraint (e.g., a 5% trailing buffer), the algorithm flags a terminal risk violation. This locks in liquidation based purely on intra-trade path dependency, independent of realized historical statements.

Why do modern proprietary firms favor trailing equity watermarks over static balance checkpoints?

Proprietary funding institutions utilize trailing watermarks as a statistical risk management tool to accelerate the probability of ruin for speculative profiles. By removing open valuation expansions from the available downside buffer, firms insulate corporate backing while restricting retail exposure parameters.

How can a quantitative algorithm optimize safety boundaries against dynamic drawdown structures?

An automated system must integrate local tracking variables that mirror the firm's strict calculation matrix. Implementing hard tracking constraints inside the execution engine, utilizing partial take-profit parameters, and adjusting stop distances systematically based on floating high-water marks prevents automated strategy liquidation.